tylerdurden

Active Member

- Joined

- Apr 4, 2010

- Messages

- 523

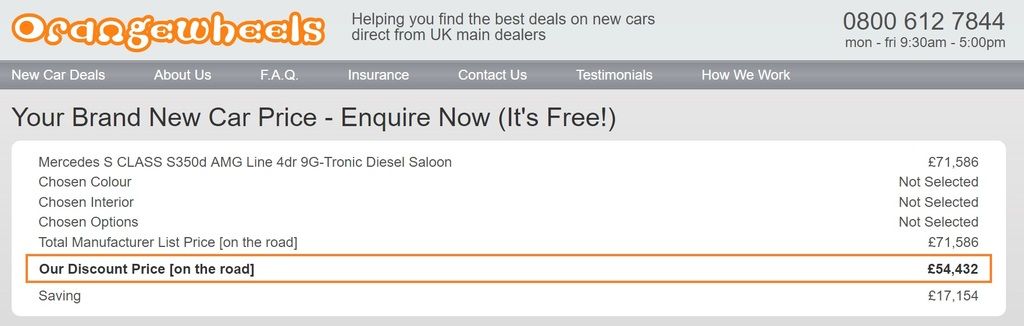

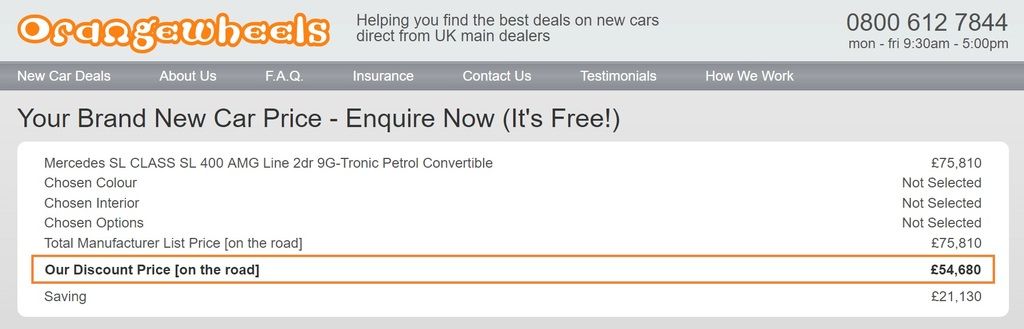

Was a a dealer this week and noted 0% on new S class. I found that quite surprising to be honest.

Do they often have 0% deals?

Is this a function of "end of line"? Or something often seen on the big cars?

Do they often have 0% deals?

Is this a function of "end of line"? Or something often seen on the big cars?

(I must stop looking.

(I must stop looking.  )

)